[RESOLVED] Where is my Money? – Fidelity

[RESOLVED]

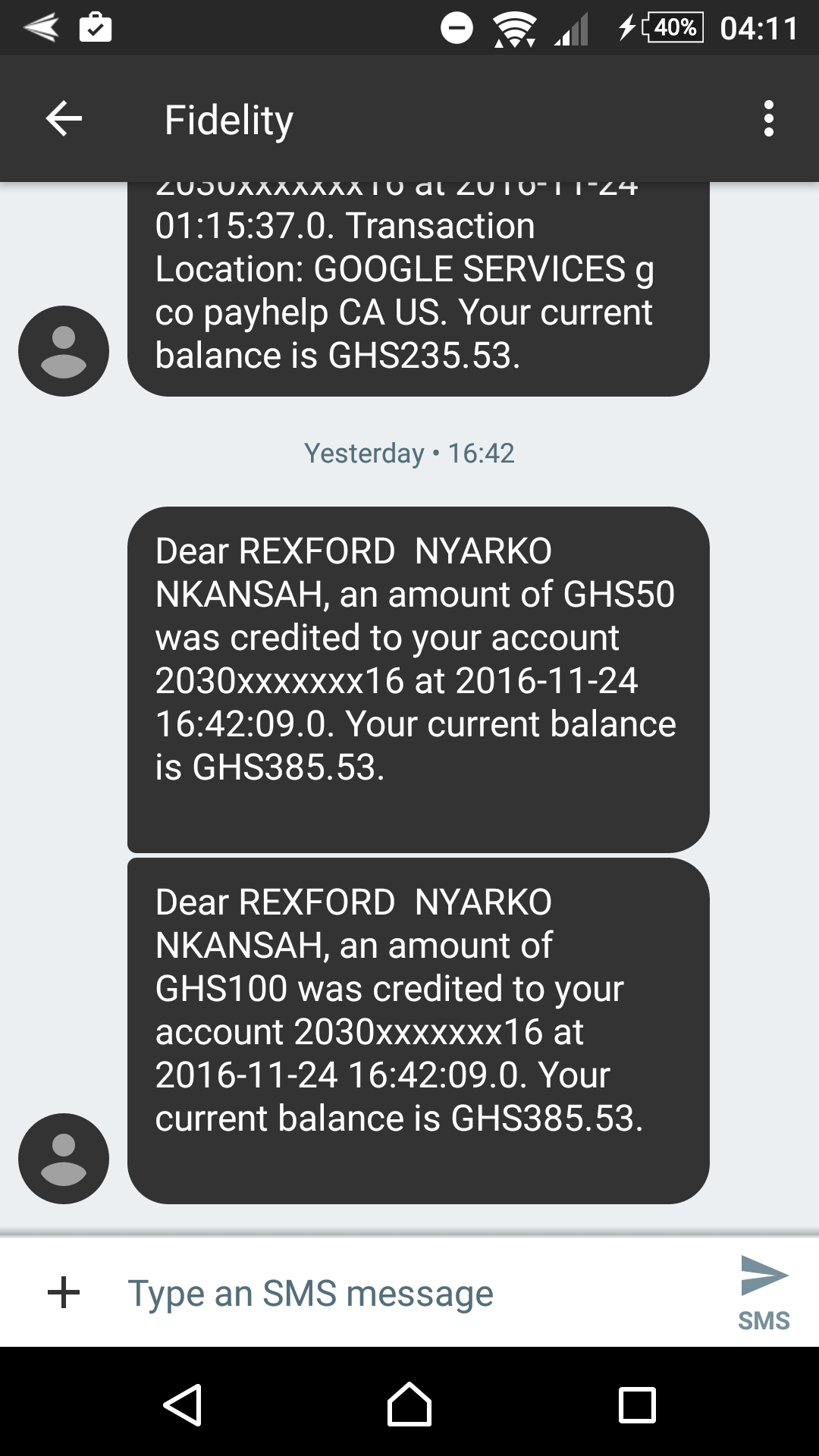

Thursday, November 24, 2016, at 16:42, my hijacked 150 cedis was safely returned home, thanks to Fidelity

Here!

As to the intricacies relating to how Fidelity resolved the issue before the 45 working days given me, it is hard for me to unravel.

However, what I do certainly know is, immediately Mr. George (from Fidelity) did ‘pay attention’ to my complaint, just a little bit, 45 working days wasn’t needed. In fact, he resolved the issue, initiated a refund and all, within less than 6 hours. You see, someone just needs to look at it, and a big thanks to George for looking at it for me.

I’m gonna live on this 150 cedis for the next 6 months, so it means a lot to me. Entering 2017 with it, crucial!

At the end of the day, it is a win-win for all involved – I got my money back, and Fidelity gets to finish their yearly auditing in peace, knowing they haven’t hijacked anyone’s money.

When Fidelity pays just a little bit of attention to your issue, it gets fixed, and no 45 working days is required. I have a feeling you’re told ’45 working days’ so that you’re off their back, so they can go about doing their other stuff.

’45 working days’ is a pretty long, long enough for your issue to be ditched peacefully. And Oh, you probably would have forgotten and went on with your life if you’re told issue is gonna take 2+ months. Kinda legit, right?

I hope not get in similar crossfires with Fidelity henceforth. I plan to do so by simply avoiding any long-winding mobile money online transactions. The money bounces off too many channels the probably of something going wrong is very high, and yes, they’ll go wrong!

Summary (and lessons)

- MPower and SlydePay had nothing to do with the issue. Fidelity didn’t handle their end of the transaction to the full, thus both merchants had no way of knowing. Since it all started with a blame game, it wasn’t clear who to trust. Now, know, SlydePay and MPower are clean! Who’s not clean? They know themselves!

- Why the heck will Fidelity wanna drag Visa’s name in the mud? Just don’t mention Visa’s name. Visa doesn’t store money. Just don’t! Fix your systems!

- When Fidelity pays attention to your issue, it can and does get fixed as soon as possible. As to how to know they’re paying attention is another unknown. As to whether your issue was even logged remains a mystery too.

- Be sure to follow up on your issues, for the teller/bank representative probably did not enter your issue into the system, or the bank reporting system might (and very like, about 92.54% sure) have failed! Heck, it happened to me. Although you deeply care about your issue, don’t assume they all automatically do feel same about your problem. In fact, in many cases, they don’t. An insult from a husby/bf or a Denial of Service (DOS attack) from the wife/gf could mean you’re just a nuissance! The fact that I could be told via email to go pick my internet banking PIN up at the branch, only to arrive to be told the PIN ain’t in, just paints the picture, how pranking the bank can be. They probably enjoy the fun of messing up with us!

- I’m done with these online transactions. Visa has NEVER failed me. Used from 3 other countries. Never failed! If it fails, it ain’t Visa, rather likely, from my bank or the merchant. And speaking of merchants, I’ve had very bad experiences with, MPower in particular previously. I’m happy to use these services for simple, little transactions, with the goal that, should it go south, I’ll be ok parting ways with the money. Otherwise, #)(#$*) you!

Will I stop using Fidelity? No! Will I recommend Fidelity to others? Maybe. Honestly, aren’t the other banks all the same? ‘The value is the same’

Will Fidelity mess up with me/you again? Oh yep, <star-wars>I have a bad feeling about that!</star-wars>. Imagine this issue happening to some 100 or 1000 people and only 1 person coming out for a refund. That is 9,900 cedis or 9,900,000 cedis.

I’m not stupid! Why would I fix my system if such sweet strayed revenue will end up in my coffers? Remember Airtel and their Sika Kokoo scandal?

As much as this system needs to be fixed, what happens to all this strayed cash that no one asked for? Some count on the excuse of the ‘brokenness’ of their system, as it serves them well!

Duh!

The article below will be left intact for reference sake!

Written: Nov 21, 2016 (Although article below makes mention of SlydePay and MPower, they weren’t the culprit. See above resolution update.

I will be thorough and detailed in this article, regarding how the proliferation of this so-called mobile-money-app-smartphone-transfer-connected-to-bank-account thing can, and in most cases, is a mess, chaos, unreliable, and money-stealing.

My issue isn’t with a one-time thing, however, a recurring scenario, I’m sure many are suffering from. At the end of this article, I suggest a better way forward, a real solution, one free from nonsense, streamlined to benefit everyone, anyone, anywhere, anytime, globally – even at the bottom-most part of the ocean – as long as there’s internet connection.

Calm Down, What’s the Issue?

In a nutshell, this is what happens:

You try to make a transaction from your MPower or Slydepay. The transaction, according to the app or vendor, says “failed”

However, the so-called failed transaction hits your bank account – in my case, Fidelity – and attempted transaction amount is deducted.

No topup is made. Vendors (Slydepay, MPower or whatever) say transaction failed, so your account on those platforms aren’t updated to reflected deducted amount from Bank account.

Bank too says, they’ve delivered the money to the vendor.

So you guessed right. The 2.5 billion dollar question is, Where is my money?

Where is my Money?

The question doesn’t get simpler than that. “Where is my money?”

Bank says it is with the merchant. Merchant says bank didn’t give to them. Who do I chase for the money? I am in a similar situation at the moment, and I believe someone isn’t telling the truth, someone is lying right to my face, and trying to indirectly tell me, “GTH! partying with your 150 cedis this weekend”.

Oh well, you can except I’m coming for it, and ALL of it!

What went down?

The above is what went down.

In summary:

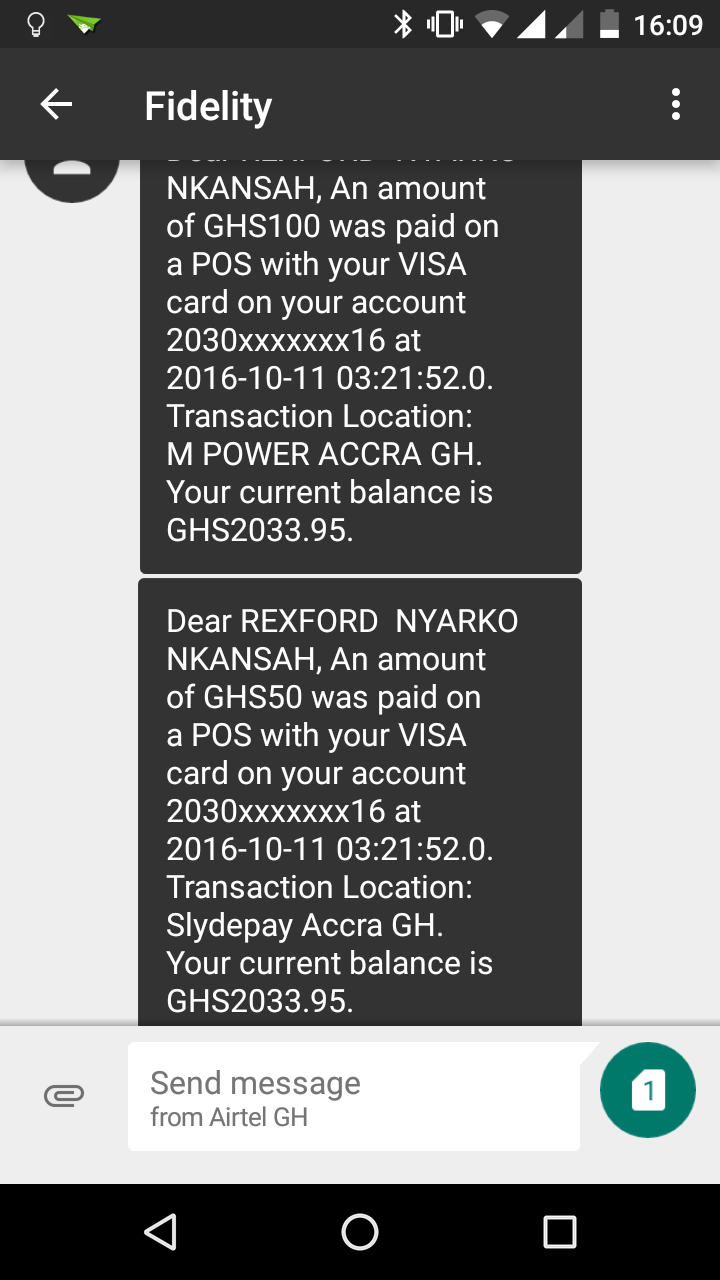

- I made a transaction of said amounts below.

- About an hour later (timestamps in above receipt), I’m told amounts have been deducted from bank account

- Merchants also say transaction failed.

Chat with Bank – Fidelity

My chat with the Fidelity lady on phone didn’t go well. She insisted my transaction has no logs in their system, and that, I’ve not even hit my bank account for the combined 150 cedis.

Like seriously? “So where did that text message come from?”, I asked her. She sounded confused, and probably didn’t even know how to go about their own system.

Walked in the next day to the A&C Mall branch. The conversation went like, ‘We see your transaction, the amount was deducted, and sent to the merchants. To Fidelity, your money ain’t with us anymore. Transaction was done, and that’s it.’

Before you go, ‘This sounds convincing!’, wait until you recheck the timestamps on the above screenshot. Notice the problem?

Two transactions, from two merchants, happened on the same date, same time, to the same milliseconds, i.e, 03:21:52.0

Oooh, that’s fishy to me. If I happened to execute both transactions, at the same exact, precise time, did the transaction not go over the airways?

In fact, I didn’t. The first transaction was Mpower, followed by Slydepay, 100 and 50 cedis respectively. I’m human (not Barry Allen), there’s no way I could create two transactions, from two apps, of two merchants at the same time, going through separate routes, reaching bank at same timestamp.

The point? What was wrong with Fidelity at that time? With such suspicious transaction feedback, aren’t they sure their system deducted amount without actually sending it?

Chat with Merchant – Slydepay & Mpower

According to both Merchants, a failed transaction unwinds automatically after some time, max 3 to 5 working days. The keyword is, *automatically!*.

In my case, that didn’t happen. When a transaction unwinds and drops back into my account, Fidelity usually notifies me. Think of it as standard protocol.

The fact that none of this automated reversal process happened clearly indicates the Bank, through Visa (I use Visa Card) got an “OK” response from these merchants, confirming money has been delivered, however, for whatever bugs in there in the merchants’ system, I’m told transaction failed, *although* Bank understands money safely delivered.

My phone/email correspondence with both Slydepay and Mpower, what they joyfully nailed into my ears was the fact that, they don’t have my money.

Slydepay Response:

“Your transaction timed out as discussed on phone the day it happened. This means that Slydepay was not able to debit your card.

As discussed on phone even though you received an sms, your bank will have a reversal done to your bank account.

Kindly get in touch with your bank and inform them about a timed out transaction so that the reversal can be done.”

“I want to assure you that the money is not with us and I just hope and pray it doesn’t take that long to have a reversal done with fidelity.After our conversation we went further to investigate and noticed that the feedback from the bank was ‘do not honor’ and this message could be as a result of a number of things.”

Possible culprits?

Opening up the playfield, at least I know of these platform/technologies involved.

- The bank, Fidelity

- Visa – tied into my bank account. Visa is the middle-man

- Mpower or Slydepay, going through Visa to touch Bank

Now, according to Visa:

“VISA handles on average around 2,000 transactions per second (tps)” – source

The point? The fault ain’t coming from Visa, because, well, it works!

Now, let’s come back to Ghana, away from the Visa guys in USA.

With Fidelity:

- The bank is errored in processing “Do not honor” requests, dispatching/deducting money although not actually sending it

- The bank sends the amount, but fails, for whatever reasons, to listen on the wire for the right error response to act upon, thus, probably an error message was returned, but since the bank didn’t intercept properly, no way to act and considers transaction a safe one.

With Mpower or Slydepay:

- An amount was received, yet didn’t process properly, leaving the system with cool 100 and 50 cedis yet without any attached account.

Conclusion

As the end user, I do not really care about what went on or who’s fault. My primary concern?

Where is My Money?

To console me, the Fidelity lady told me:

‘Normally, these transactions take about 45 working days to be resolved. So please wait until then. In the mean time, please file this report and we shall send in to the Cards department.’

Interestingly, that was my second time filling a complaint relating to my card, however for a previous transaction, in which my 20 cedis also vanished into thin air. Wondering what happened? Never got my money back!

By the way, Oh dear, 45 working days? Is that a lie?

Now some 20 working days away from day transaction failed. Fingers crossed. Until this issue is resolved, my money given back to me, I’m not using any of these bad money transaction systems popping up everywhere in Ghana these days.

Quack developers are employed who simply have no basic understanding of Atomic Transactions, who end up writing what Root of Person of Interest calls, “Bad Code”. Code so bad, it ends up causing financial loss to already broken individuals like myself.

Shame onto whoever is behind the development of the Fidelity Bank and the developing of MPower and Slydepays. My respect for you guys drops, crashes through the ground, leaving a 2-mile hole!

There’s a huge difference between writing a fun project, and handling financial transactions. With mission-critical tasks, no margin of error available, unlike any pet, hobby project.

As it stands now, I’m still asking the 150 Cedis question: “Where is My Money?”